Understanding Personal Loans in the US: Everything You Need to Know

What is a Personal Loan?

A personal loan is a type of unsecured or secured loan that allows individuals in the United States to borrow a fixed amount of money from a bank, credit union, or online lender. Unlike mortgages or auto loans, personal loans are typically unsecured, meaning they do not require collateral. Borrowers repay the loan in fixed monthly installments over a period ranging from 1 to 7 years depending on the lender and loan terms.

Personal loans are highly versatile and can be used for purposes such as debt consolidation, medical bills, home renovations, or even large purchases. Understanding how they work, their eligibility criteria, and the associated costs is crucial before applying.

How Personal Loans Work in the US

When you apply for a personal loan in the US, lenders evaluate your credit score, income, employment history, and debt-to-income ratio to determine whether you qualify and the interest rate you will receive. Once approved, you receive a lump sum amount and agree to repay it in monthly installments, which include both principal and interest.

Most personal loans in the US are fixed-rate loans, meaning the interest rate remains the same throughout the loan term. Some lenders also offer variable-rate loans, which fluctuate with market interest rates.

Types of Personal Loans

Secured vs Unsecured:

- Secured Loans: Require collateral such as a car or savings account. They often have lower interest rates due to reduced risk for the lender.

- Unsecured Loans: Do not require collateral. They are riskier for lenders, so interest rates are usually higher.

Fixed-rate vs Variable-rate:

- Fixed-rate Loans: The interest rate stays constant over the life of the loan, making it easier to budget.

- Variable-rate Loans: Interest rates can change, potentially saving money if rates decrease, but they carry the risk of higher payments if rates rise.

Eligibility Criteria for Personal Loans in the US

While requirements vary by lender, common eligibility factors include:

- Credit Score: Typically 620+ for unsecured loans. Higher scores may get better rates.

- Income: Steady income to demonstrate repayment ability.

- Employment History: Proof of stable employment increases approval chances.

- Debt-to-Income Ratio: Lenders usually prefer a ratio below 40%.

- Age and Residency: Must be at least 18 years old and a US citizen or permanent resident.

Interest Rates and Fees: What to Expect

Interest rates on personal loans in the US typically range from 6% to 36%, depending on creditworthiness and loan type. Fees may include:

- Origination Fee: 1% to 6% of the loan amount.

- Late Payment Fee: Charged for missed payments.

- Prepayment Penalty: Some lenders charge for early repayment.

How to Apply for a Personal Loan

1. Check Your Credit Score: Know your score and correct any errors.

2. Compare Lenders: Look for competitive interest rates and terms.

3. Pre-Qualification: Many online lenders offer pre-qualification without affecting your credit score.

4. Submit Application: Provide personal, employment, and financial information.

5. Receive Funds: Once approved, the loan is typically disbursed within a few days.

Pros and Cons of Personal Loans

Pros:

- Quick access to funds.

- Flexible usage.

- Fixed monthly payments make budgeting easier.

Cons:

- High-interest rates for low credit scores.

- Potential for over-borrowing.

- Late payments can negatively affect credit score.

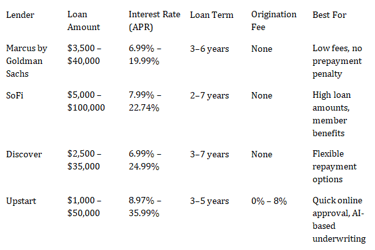

Table: Comparison of Top Personal Loan Providers in the US

Tips for Managing and Repaying Your Loan

- Set up automatic payments to avoid late fees.

- Pay more than the minimum to reduce interest.

- Avoid taking multiple loans simultaneously.

- Keep track of your debt-to-income ratio to maintain healthy credit.

FAQs: Common Questions About Personal Loans

1. Can I get a personal loan with bad credit?

Yes, but interest rates will be higher, and loan amounts may be smaller. Consider credit unions or online lenders specializing in bad credit loans.

2. How long does it take to get a personal loan in the US?

Online lenders can approve and disburse funds within 1–5 business days, while traditional banks may take longer.

3. Can I pay off my personal loan early?

Most lenders allow early repayment without penalties, but always confirm with your lender.

4. What is the average personal loan interest rate in the US?

Rates vary widely, from around 6% for borrowers with excellent credit to 36% for high-risk borrowers.

5. Are personal loans taxable?

No, personal loans are not considered taxable income in the US.

Conclusion: Is a Personal Loan Right for You?

Personal loans in the US can be a powerful tool for consolidating debt, financing major expenses, or improving cash flow. However, it’s crucial to understand your eligibility, interest rates, fees, and repayment obligations. By carefully comparing lenders and borrowing responsibly, you can maximize the benefits while minimizing the risks.

Comparison of Top Personal Loan Providers in the US